This AI chip stock is trading at an incredibly cheap valuation despite growing at a terrific pace.

The semiconductor industry has received a massive boost in the past three years thanks to the advent of artificial intelligence (AI), and that’s not surprising, as semiconductors provide the basic building blocks for the proliferation of AI.

From AI model training, to inference, to running AI applications in the cloud, to powering AI devices such as smartphones and computers, chips are needed at nearly every juncture for using this technology. This explains why several chipmakers have been witnessing healthy growth in their revenue and earnings in recent years.

Image source: Getty Images.

Marvell Technology (MRVL 0.23%) is one such semiconductor stock that has been growing at a nice clip on the back of solid demand for its application-specific integrated circuits (ASICs), which are being deployed in AI data centers. More importantly, investors can buy Marvell stock at an incredibly cheap valuation right now.

Let’s look at the reasons why Marvell looks like one of the most undervalued semiconductor stocks you can buy right now.

Marvell is incredibly cheap despite its phenomenal growth

Marvell’s growth has taken off remarkably in the past year. This is evident from the chart below.

MRVL Revenue (Quarterly) data by YCharts

The company’s data center business has played a central role in driving this stunning turnaround, helping it overcome the poor performance of its other business segments that were under severe stress last year. Marvell management remarked on the company’s May earnings conference call that “the rapid scaling of our custom AI silicon programs to high-volume production, along with robust shipments of our electro-optics products for AI and cloud applications” are the reasons why its growth has been outstanding of late.

Specifically, the company’s revenue shot up an impressive 63% year over year in the first quarter of its fiscal 2026 (ended on May 3) to $1.89 billion. Meanwhile, its adjusted earnings jumped 158% year over year to $0.62 per share. You will be amazed to know that Marvell stock is trading at just 22 times earnings despite posting such a healthy jump in its top and bottom lines last quarter.

What’s more, its guidance of $2 billion in revenue and $0.67 per share in non-GAAP (adjusted) earnings for the recently concluded fiscal Q2 points toward another quarter of stunning growth. Its earnings are on track to more than double once again, and that makes buying Marvell a no-brainer considering its cheap valuation.

Even better, Marvell has the ability to sustain its elevated growth levels in the long run.

Why this chip company is built for impressive long-term growth

Demand for ASICs, or custom AI processors, which Marvell designs, is growing rapidly. That’s because these custom AI processors can help hyperscalers significantly reduce operating costs since they are designed for performing specific tasks that they can execute with higher efficiency and lower power consumption when compared to graphics processing units (GPUs).

As a result, cloud computing giants such as Amazon, Alphabet, Microsoft, and Meta Platforms are some of the big names that have been tapping custom AI chip designers such as Marvell and Broadcom to produce in-house chips. The good part is that Marvell already counts the likes of Amazon, Alphabet, and Microsoft as customers, which is the reason why its growth has been impressive of late.

Moreover, Marvell is expecting the custom AI chip market to open up an addressable opportunity worth $55 billion by 2028 as compared to just $6.6 billion in 2023. The company is well placed to capitalize on this opportunity as it currently has a pipeline of 10 customers for whom it is designing 18 chips, up from just four one year ago. Looking ahead, Marvell expects its chip design pipeline to increase to 50.

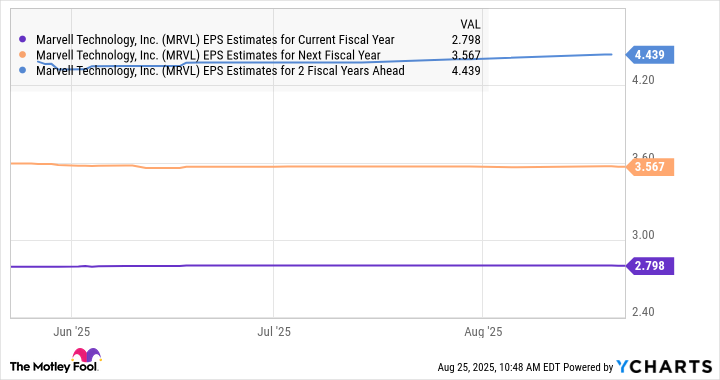

So, it is easy to see why Marvell’s earnings are estimated to increase at a nice pace.

MRVL EPS Estimates for Current Fiscal Year data by YCharts

This AI stock is probably one of the most undervalued names in the semiconductor sector that investors can buy right now. And doing so could turn out to be a profitable move as Marvell’s healthy earnings growth could be rewarded with a premium earnings multiple, paving the way for solid stock price upside.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Amazon, Meta Platforms, and Microsoft. The Motley Fool recommends Broadcom and Marvell Technology and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Great Job newsfeedback@fool.com (Harsh Chauhan) & the Team @ The Motley Fool Source link for sharing this story.

{kind=link}