Last year, China started construction on an estimated 95 gigawatts (GW) of new coal power capacity, enough to power the entire UK twice over.

It accounted for 93% of new global coal-power construction in 2024.

The boom appears to contradict China’s climate commitments and its pledge to “strictly control” new coal power.

The fact that China already has significant underused coal power capacity and is adding enough clean energy to cover rising electricity demand also calls the necessity of the buildout into question.

Furthermore, so much new coal capacity provides an easy counterargument for claims that China is serious about the energy transition.

Did China really need more coal power?

And now that it is here, do all these brand-new power plants mean China’s greenhouse gas emissions will remain elevated for longer?

This article addresses four common talking points surrounding China’s ongoing coal-power expansion, explaining how and why the current wave of new projects might come to an end.

New coal is not needed for energy security

The explanation for China’s recent coal boom lies in a combination of policy priorities, institutional incentives and system-level mismatches, with origins in the widespread power shortages China experienced in the early 2020s.

In 2021, a “mismatch” between the price of coal and the government-set price of coal-fired power incentivised coal-fired power plants to cut generation. Furthermore, power shortages in 2020 and 2022 revealed issues of inflexible grid management and limited availability of power plants, when demand spiked due to extreme weather and elevated energy-intensive economic activity, compounded by coal shortages, reduced hydro output and insufficient imported electricity import.

Following this, energy security became a top priority for the central government. Local governments responded by approving new coal-power projects as a form of insurance against future outages.

Yet, on paper, China had – and still has – more than enough “dispatchable” resources to meet even the highest demand peaks. (Dispatchable sources include coal, gas, nuclear and hydropower.) It also has more than enough underutilised coal-power capacity to meet potential demand growth.

A bigger factor behind the shortages was grid inflexibility. During both the 2020 power crisis in north-east China and the 2022 shortage in Sichuan, affected provinces continued to export electricity while experiencing local shortages.

A lack of coordination between provinces and inflexible market mechanisms governing the “dispatch” of power plants – the instructions to adjust generation up or down – meant that existing resources could not be fully utilised.

Nevertheless, with coal power plants cheap to build and quick to gain approval, many provinces saw them as a reliable way to reassure policymakers, balance local grids and support industry interests, regardless of whether the plants would end up being economically viable or frequently used.

China’s average utilisation rate of coal power plants in 2024 was around 50%, meaning total coal-fired electricity generation could rise substantially without the need for any new capacity.

At the same time as adding new coal, the Chinese government also addressed energy security through improvements to grid operation and market reforms, as well as building more storage.

The country added dozens of gigawatts of battery storage, accelerated pumped hydro projects and improved trading linkages between electricity markets in different provinces.

Though these investments could have gone further, they have already helped avoid blackouts during recent summers – when few of the newly-permitted coal power plants had come online. As such, it is not clear that the new coal plants were needed to guarantee security of supply in the first place.

President Xi Jinping has stated that “energy security depends on developing new energy” – using the Chinese term for renewables excluding hydropower and sometimes including nuclear. According to the International Energy Agency, in the long run, resilience will come not from overbuilding coal, but from modernising China’s power system.

New coal power plants do not mean more coal use and higher emissions

It may seem intuitive to imagine that if a country is building new coal power plants, it will automatically burn more coal and increase its emissions.

But adding capacity does not necessarily translate into higher generation or emissions, particularly while the growth of clean energy is still accelerating.

Coal power generation plays a residual role in China’s power system, filling the gap between the power generated from clean energy sources – such as wind, solar, hydro and nuclear – and total electricity demand. As clean-energy generation is growing rapidly, the space left for coal to fill is shrinking.

From December 2024, coal power generation declined for five straight months before ticking up slightly in May and June, mainly to offset weaker hydropower generation due to drought. Coal power generation was flat overall in the second quarter of 2025.

The chart below shows growth in monthly power generation for coal and gas (grey), solar and wind (dark blue) and other low-carbon power sources (light blue).

This illustrates how the rise in wind and solar growth is squeezing the residual demand left for coal power, resulting in declining coal-power output during much of 2025 to date.

Another way to consider the impact of new coal-fired capacity is to test whether, in reality, it automatically leads to a rise in coal-fired electricity generation.

The top panel in the figure below shows the annual increase in coal power capacity on the horizontal axis, relative to the change in coal-power output on the vertical axis.

For example, in 2023, China added 47GW of new coal capacity and coal power output rose by 3.4TWh. In contrast, only 28GW was added in 2021, yet output still rose by 4.4TWh.

In other words, there is no correlation between the amount of new coal capacity and the change in electricity generation from coal, or the associated emissions, on an annual basis.

Indeed, the lower panel in the figure shows that larger additions of coal capacity are often followed by falling utilisation. This means that adding coal plants tends to mean that the coal fleet overall is simply used less often.

As such, while adding new coal plants might complicate the energy transition and may increase the risk of unnecessary greenhouse gas emissions, an increase in coal use is far from guaranteed.

If instead, clean energy is covering all new demand – as it has been recently – then building new coal plants simply means that the coal fleet will be increasingly underutilised, which poses a threat to plant profitability.

China is not unique in its approach to coal power

The dynamics behind last year’s surge in coal power project construction starts speak to the logic of China’s system, in which cost-efficiency is not always a central concern when ensuring that key problems are solved.

If a combination of three tools – coal power plants, storage and grid flexibility, in this case – can solve a problem more reliably than one alone, then China is likely to deploy all three, even at the risk of overcapacity.

This approach reflects not just a desire for reliability, but also deeper institutional dynamics that help to explain why coal power continues to be built.

But that does not mean that such a pattern is unique to China.

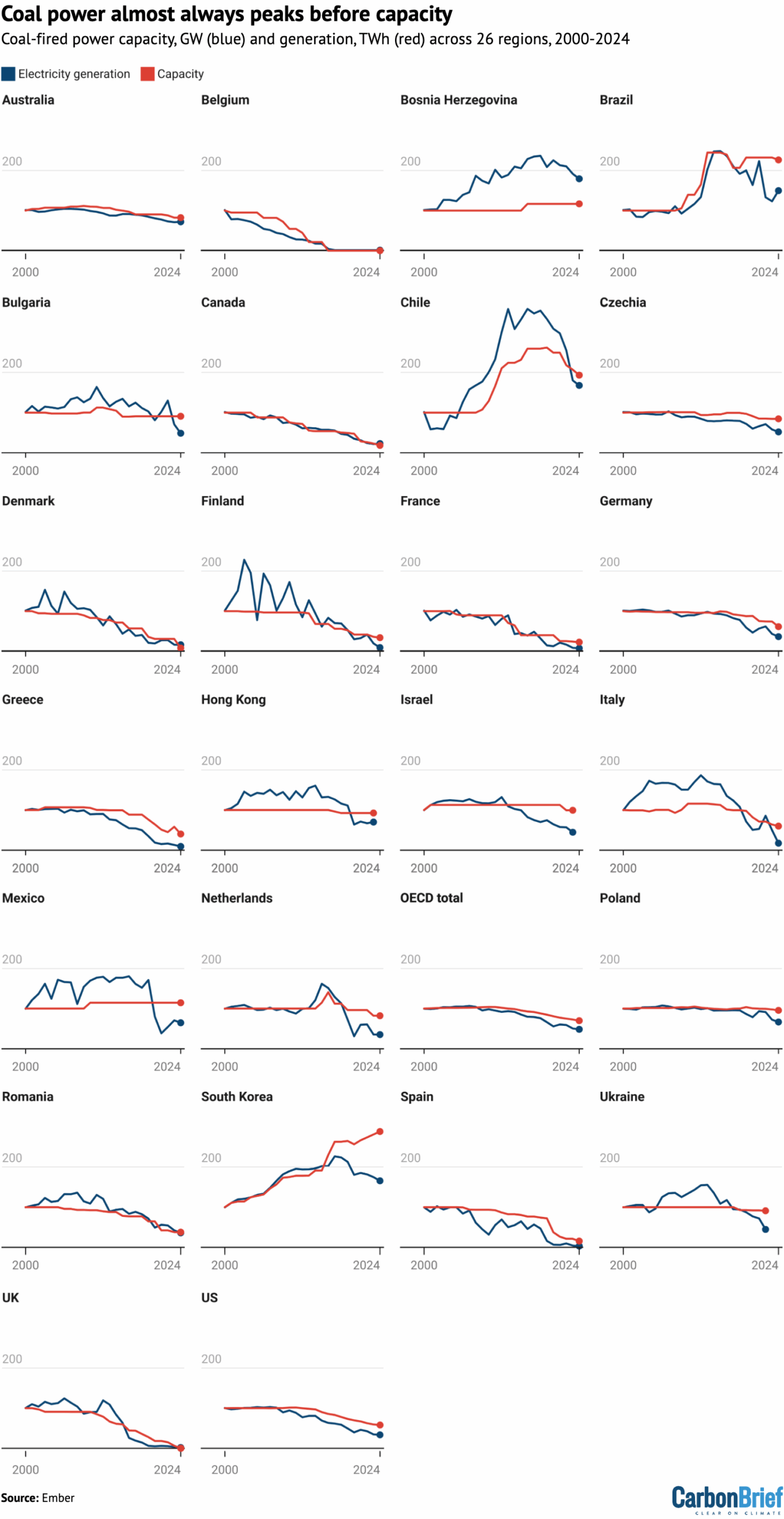

The figure below shows that, across 26 regions, a peak in coal-fired electricity generation (blue lines) almost always comes before coal power capacity (red) starts to decline.

Moreover, the data suggests that once there has been a peak, generation falls much more sharply than capacity, implying that remaining coal plants are kept on the system even as they are used increasingly infrequently.

In most cases, what ultimately stopped new coal power projects in those countries was not a formal ban, but the market reality that they were no longer needed once lower-carbon technologies and efficiency gains began to cover demand growth.

Coal phase-out policies have tended to reinforce these shifts, rather than initiating them. In China, the same market signals are emerging: clean energy is now meeting all incremental demand and coal power generation has, as a result, started to decline.

Coal is not yet playing a flexible ‘supporting’ role

Since 2022, China’s energy policy has stated that new coal-power projects should serve a “supporting” or “regulating” role, helping integrate variable renewables and respond to demand fluctuations, rather than operating as always-on “baseload” generators.

More broadly, China’s energy strategy also calls for coal power to gradually shift away from a dominant baseload role toward a more flexible, supporting function.

These shifts have, however, mostly happened on paper. Coal power overall remains dominant in China’s power mix and largely inflexible in how it is dispatched.

The 2022 policy provided local governments with a new rationale for building coal power, but many of the new plants are still designed and operated as inflexible baseload units. Long-term contracts and guaranteed operating hours often support these plants to run frequently, undermining the idea that they are just backups.

Old coal plants also continue to operate under traditional baseload assumptions. Despite policies promoting retrofits to improve flexibility, coal power remains structurally rigid.

Technical limitations, long-term contracts and economic incentives continue to prevent meaningful change. Coal is unlikely to shift into the flexible supporting role that China says it wants without deeper reform to dispatch rules, pricing mechanisms and contract structures.

Despite all this, China is seeing a clear shift away from coal. Clean-energy installations have surged, while power demand growth has moderated.

As a result, coal power’s share in the electricity mix has steadily declined, dropping from around 73% in 2016 to 51% in June 2025. The chart below shows the monthly power generation share of coal (dark grey), gas (light grey), solar and wind (dark blue), and other low-carbon sources (light blue) from 2016 to the present.

When will the coal boom end?

About a decade ago, the end of China’s coal power expansion also looked near. Coal power plant utilisation declined sharply in the mid-2010s as overcapacity worsened. In response, the government began restricting new project approvals in 2016.

With new construction slowing and power demand rebounding, especially during and after the height of the Covid-19 pandemic, utilisation rates recovered. Not long after, power shortages kicked off the recent coal building spree.

Now, there are new signs that the coal power boom is approaching its end. Permitting is becoming more selective again in some regions, especially in eastern provinces where demand growth is slowing and clean energy is surging. Meanwhile, system flexibility is advancing.

Compared to the late 2010s, the current shift appears more structural. It is driven by the rapid expansion of clean energy, which increasingly eliminates the need for large-scale new coal power projects.

Still, the pace of change will depend on how quickly institutions adapt. If grid operators become confident that peak loads can reliably be met with renewables and flexible backup, the rationale for new coal power plants will weaken.

Equally important, entrenched interests at the provincial and corporate levels continue to push for new plants, not just as insurance, but as sources of investment, employment and revenue. Through long-term contracts and utilisation guarantees, this represents institutional lock-in that may delay the shift away from coal.

The next major turning point will come when coal power utilisation rates begin to fall more sharply and persistently. With large amounts of capacity set to come online in the next two years and clean energy steadily displacing coal in the power mix, a sharp drop in coal power plant utilisation appears likely.

Once this happens, the central government might be expected to step in through administrative capacity cuts – forcing the oldest plants to retire – just as it did during overcapacity campaigns in the steel, cement and coal sectors around 2016 and 2017.

In that sense, China’s coal power phase-out may not begin with a single grand policy declaration, but with a familiar pattern of centralised control and managed retrenchment.

A key question is how quickly institutional incentives and grid operation will catch up with the dawning reality of coal being squeezed by renewable growth, as well as whether they will allow clean energy to lead, or continue to be held back by the legacy of coal.

The upcoming 15th five-year plan presents a crucial test of government priorities in this area. If it wants to bring policy back in line with its long-term climate and energy goals, then it could consider including clear, measurable targets for phasing down coal consumption and limiting new capacity, for example.

While China’s coal power construction boom looks, at first glance, like a resurgence,it currently appears more likely to be the final surge before a long downturn. The expansion has added friction and complexity to China’s energy transition, but it has not reversed it.

Great Job Carbon Brief Staff & the Team @ Carbon Brief Source link for sharing this story.

{kind=link}